CPG Trends Continue to Deteriorate

General Mills cut its fiscal 2025 guidance virtually across the board owing to higher price promotions

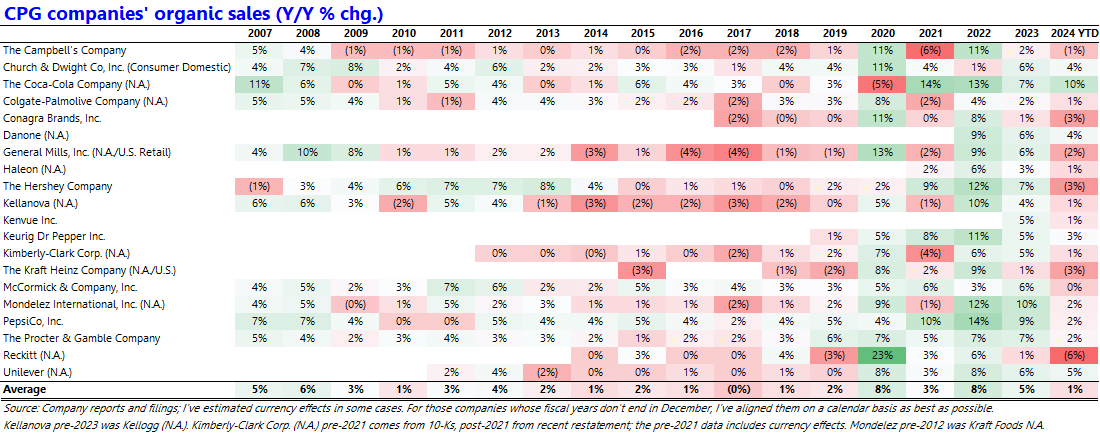

I’ve written about chronically weak sales trends among U.S. retailers, restaurant chains and consumer packaged goods (CPG) companies in recent quarters despite continued above-trend GDP growth; much of the latter is coming from historically elevated government spending and health care spending. The weakness among consumer companies shows no signs of abating. General Mills was the first CPG company to report post-October results (its fiscal 2Q25 ended in November), and the company reduced its fiscal 2025 sales and profit guidance. General Mills now expects its organic sales to be at the lower end of its previously guided range of flat to up 1% (meaning flat sales this year), and its adjusted operating profit to fall by 2-4% compared to its previous expectation of flat to down 2%. Why? Higher price promotions than initially planned amid a “challenging macroeconomic backdrop.”

I’ve noted that CPG companies raised their prices dramatically during the pandemic, and their volumes have been under continuous downward pressure over the past two years as a result. In response, companies such as General Mills are promoting more to try to boost demand.

The tables below, in which I focus on the North American market to the extent possible, illustrate what transpired during the pandemic. Ten of the largest CPG companies raised prices (price/mix to be precise) by an average of 24% over the past four years, dwarfing their price increases over any other period since 2007. Consequently, their volumes have been falling such that their organic sales growth has slowed to just 1% this year, the lowest annual rate since 2018. An obvious question is where from here given the magnitude of the cumulative price increases; I think General Mills’ commentary is a sign of what’s to come in consumer land (more price promotions to try to boost demand).

It’s not as though CPG companies raised prices by much more than CPI, either; cumulative CPI has been 20% since 2021, compared to the CPG companies’ price increases of 24%. If the CPG companies are having to effectively cut prices via higher promotions, what will most other consumer companies do over the next year, other than those selling essential items such as drugs (the sales of which have been growing rapidly)?