Health Care Accounts For ~50% of U.S. Consumer Spending Growth

Economic prosperity in the form of GLP-1 and other drug spending?

I’ve written about fast-growing prescription drug sales at the likes of Walmart, CVS Health and Walgreens Boots Alliance. The trend is broader than that. Kroger, the largest U.S. supermarket chain, attributed its 1.2% identical (ID) sales growth excluding fuel in 2Q to strength in its “Health and Wellness” (pharmacy) sales among other factors; such sales were higher than the company expected but profitability was worse, the latter the result of robust GLP-1 sales. Albertsons, with which Kroger is trying to merge, is experiencing similar trends: its ID sales excluding fuel were up 2.5% in 2Q, “with strong growth in pharmacy sales driving the identical sales increase.” Strong indeed: its pharmacy sales were up a whopping 22.5%, while all other categories were essentially flat. And like Kroger, the outsized pharmacy growth is having an adverse impact on its margins; its pharmacy sales have lower gross margins than other categories. The composition of Walmart’s 3Q U.S. comparable sales growth was similar to that of Albertsons: its “Health & Wellness” (pharmacy) sales were up by a mid-teens percentage, with GLP-1 sales contributing 1 point of segment comp growth, while its other categories were up low single-digits (general merchandise) and mid single-digits (grocery), respectively.

The rapid pharmacy/drug sales growth is coming at a cost for CVS and Walgreens just as it is for Kroger and Albertsons. Walgreens noted “continued net reimbursement pressure including brand inflation and mix impacts” (its adjusted operating income in its U.S. Retail Pharmacy business fell by 60.4% in the fiscal year ended August 31, 2024, partly the result of reimbursement pressure), and CVS noted “continued pharmacy reimbursement pressure.” Wrote CVS in its latest 10-Q filing, “The segment’s adjusted operating income has been adversely affected by the efforts of managed care organizations, PBMs and governmental and other third-party payors to reduce their prescription drug costs, including the use of restrictive networks, as well as changes in the mix of business within the pharmacy portion of the Pharmacy & Consumer Wellness segment. If the pharmacy reimbursement pressure accelerates, the segment may not be able to grow revenues, and its adjusted operating income could be adversely affected.” Walgreens noted many of the same issues in its latest 10-K filing, and added that “The Company’s pharmacy business is subject to ongoing prescription reimbursement pressure, a shift in the fulfillment of prescriptions every thirty days towards 90-day at retail, an increased volume of Medicare Part D prescriptions and increased consumer use of prescription discount cards. Further consolidation among generic manufacturers coupled with changes in the number of major brand name drugs anticipated to undergo a conversion from branded to generic status may also result in gross margin pressures within the industry.” As for who’s benefiting from the rapid growth in drug sales other than the GLP-1 makers, then, that’s beyond the scope of this post (and my knowledge base).

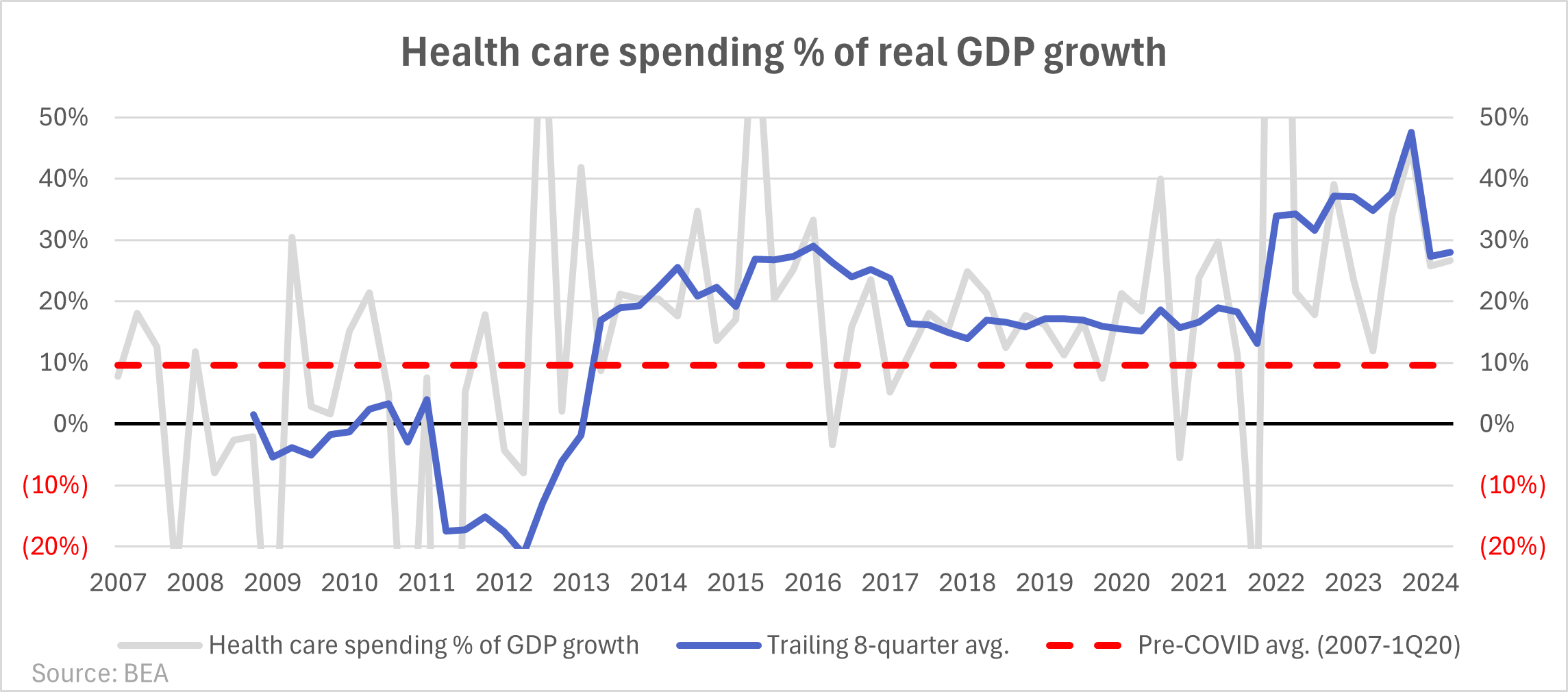

The Bureau of Economic Analysis (BEA) pointed out growing prescription drug spending in its 3Q GDP release: the “other nondurable goods” category was the single biggest contributor to consumer spending/PCE growth, and that category’s growth was led by prescription drugs (housed within “Pharmaceutical and other medical products”). Another of the biggest contributors to consumer spending growth in 3Q was health care services, led by outpatient services. In the last two years, total health care spending (the components of which can be found here) has accounted for ~50% of real (inflation-adjusted) PCE growth, roughly double the ~23% of real PCE that health care spending comprises. When economic observers talk about “strong” consumer spending growth, what they’re really referring to is spending on drugs, health care services and health insurance, whether they realize it or not; no other major component of PCE has grown nearly as quickly.