The Shifting Central Bank Sands

BIS: “It is essential to resist pressures to use monetary policy to stabilize financial markets.”

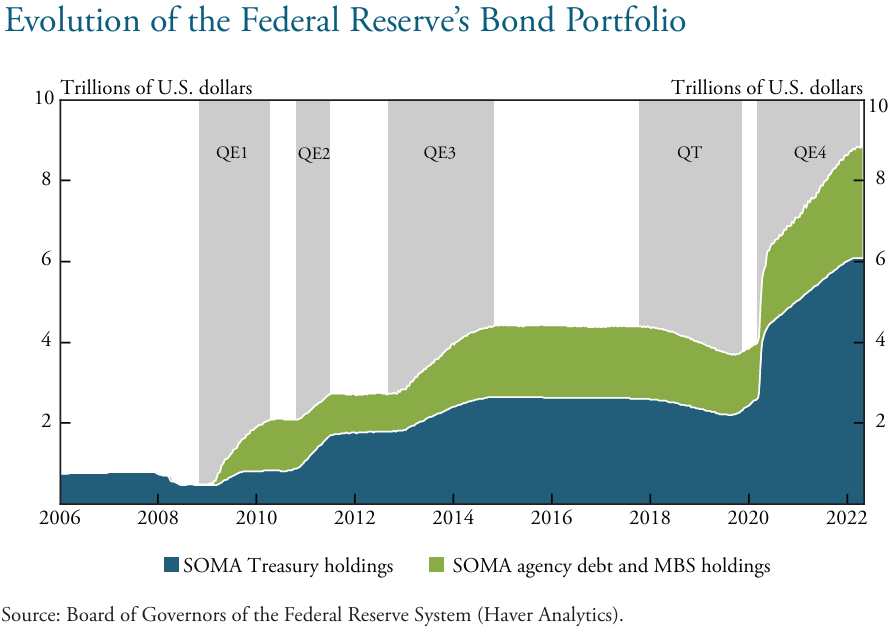

Since the Great Financial Crisis (GFC) in 2007-2009, the playbook for many developed economy central banks has been consistent: during times of crisis, lower policy rates to near-zero or zero levels and purchase government bonds and other assets such as mortgage-backed securities and corporate bonds (a process known as quantitative easing, or QE), and even after the crisis, remain more accommodative than was the case pre-crisis in the form of much larger balance sheets (both on an absolute basis and as a percentage of GDP). The chart below shows the evolution of the Federal Reserve’s balance sheet/securities holdings over the past two decades to the peak of the most recent QE program (QE4); the story is much the same for other major central banks.

Central bankers have acknowledged this unprecedented stimulus has contributed to elevated asset prices (along with 40-year high inflation in developed markets), and noted that indeed, higher asset prices are one of the key objectives of QE. Some market observers appear to operate under the assumption that central banks will be similarly accommodative in future crises. Central bankers themselves have been indicating otherwise in recent days/months, which I think warrants more attention than it’s been receiving.

Who matters in the world of central banking, and what are they saying?

When discussing global central banks, there are a few entities of particular import. The International Monetary Fund (IMF) provides central banks with policy advice. The Bank for International Settlements (BIS) is known as the central bank of central banks; it’s owned by member central banks, with its primary goal to foster international monetary and financial cooperation. And the Federal Reserve (Fed) is the world’s most important central bank.

I mention these entities in the context of recent papers/speeches that were illuminating. Last May, the IMF published a working paper titled “New Perspectives on Quantitative Easing and Central Bank Capital Policies.” While the title may not get too many pulses racing, the content was far from soporific. The IMF noted that central banks have come under growing criticism for large balance sheet losses associated with QE, and acknowledged that QE helped fuel the historic inflation surge following the pandemic. Regarding the issue of balance sheet losses, “While central banks can operate with realized losses and negative capital, the public backlash against these losses can be difficult to manage. In some cases, a weak central bank balance sheet or persistent decline in its remittances to the treasury could potentially undermine central bank credibility and independence.”

As an example, U.S. government deficits are as large as they are in part because the Fed isn’t sending any remittances to the Treasury as its costs exceed its income: the Fed is paying more interest on reserve balances, interest on reverse repos, etc. than it’s earning on the securities it bought via QE in recent years at low rates. As the FRED website notes, the Fed’s income normally exceeds its operating costs, and by law, the Fed’s excess earnings must be turned over to the Treasury as remittances. From 2012 to 2021, the Fed remitted over $800 billion to the Treasury. However, the story since has been decidedly different. The chart below shows the Fed’s cumulative operating losses since September 2022 (called a “deferred asset,” oddly enough) after the Fed rapidly raised its policy rate and its interest costs went skyward. The Fed won’t resume sending remittances to the Treasury until it pays down the value of the $221 billion deferred asset to zero.

Along similar lines as what the IMF wrote, Agustίn Carstens of the BIS gave a speech at the Federal Reserve Bank of St. Louis last week on lessons learned and challenges ahead for monetary policy. He noted that many major central banks, including the Fed, are conducting reviews of their monetary policy frameworks; the last such reviews took place in 2020-2021, right before “the greatest inflation surge since the 1970s.” Inflation was a major focus of his; he noted that “the post-pandemic experience calls for greater caution in letting inflation rise above target, given that it may surge much more strongly and swiftly than warranted.” Regarding QE, “Central banks could use greater caution in deploying their balance sheets. While asset purchases are crucial during periods of acute financial distress to preserve financial stability and strengthen monetary policy transmission, their use outside of crisis episodes is less clear. Large-scale asset purchases face diminishing marginal returns in stimulating the economy, cannot be unwound rapidly without raising financial stability concerns and may expose central banks to large financial losses…it is essential to resist pressures to use monetary policy to stabilize financial markets.”

Just a few days earlier, the Governor of the Bank of France gave a speech in which he said that QE isn’t appropriate under certain circumstances (when the primary objective is to inject liquidity), and when central banks deem it appropriate (when the primary goal of QE is transmission or financial stability), there’s no reason to hold the assets purchased to maturity or to take excessive duration risk. When the primary objective is to provide liquidity, he said “it should not be done through purchases of long-term bonds, but by lending short term or at floating rates for LTROs [a lending scheme by the ECB called longer-term refinancing operations].”

Those remarks echo what Isabel Schnabel, a member of the European Central Bank’s (ECB) Executive Board, said in a speech last year when discussing the benefits and costs of QE/asset purchases. She noted, “In a bank-based economy like the euro area…other measures, such as targeted longer-term refinancing operations, can provide substantial support to the economy in the face of disinflationary shocks and instability, while leaving a smaller and less persistent footprint, as they can be reversed more quickly if conditions change.”

What about the Fed?

Central bankers’ recent emphasis on lending operations isn’t limited to Europe. Last year, the Fed solicited feedback on operational frictions associated with the discount window as part of an effort to increase banks’ willingness to borrow from it. (The discount window is a Fed lending facility that provides banks with backup funding against a broad range of collateral. The collateral is valued at market value, as opposed to the Fed’s Bank Term Funding Program (BTFP) in which collateral was valued at par regardless of its market value at the time. Consequently, the BTFP enabled banks to borrow more against the same collateral.) As the New York Fed acknowledged in a staff report in November, there’s a stigma associated with borrowing at the window, which the institution is attempting to address.

At the same time as the Fed is trying to do so, its balance sheet continues to shrink. In recent months, market participants including the Treasury Borrowing Advisory Committee (TBAC) have been pushing out their forecasts for an end to the Fed’s quantitative tightening (QT)/balance sheet reduction program. Wrote the TBAC last week, “Dealers now see the Federal Reserve’s balance sheet reduction ending in the summer, rather than the spring, slightly increasing the expected need for borrowing from the private sector in 2025. It was noted that market participants viewed risks as skewed towards a later finish (even as far out as Q1 CY 2026), or to a multi-step wind down of QT, as reserves are seen as ample.”

In fact, they’re seen as abundant, which the Fed reiterated in an economic research piece on January 31 titled “Market-Based Indicators on the Road to Ample Reserves.” The piece was notable in that the Fed provided four readily observable indicators that the public can track in the Fed’s journey to “ample” reserve conditions (from “abundant” currently). The first indicator is something called the EFFR-IORB spread (please see here for more details). What struck me is that when calculating it, the Fed has chosen to exclude month ends along with one day before and after. Why does that matter? Some fixed income market observers have been expecting the Fed to stop its QT program partly because of increasing volatility in overnight repurchase agreement (repo) rates around financial reporting dates such as quarter-end, as shown in the chart below; the chart was part of a presentation that Roberto Perli, the person responsible for the implementation of monetary policy at the NY Fed, gave in November.

Mr. Perli acknowledged this quarter-end pressure in his speech, but nonetheless said “it does not on its own indicate that reserve supply is anything other than abundant – particularly given the message embedded in the other indicators I mentioned previously.” Furthermore, central bankers including the Fed are aware of the impact that banks’ “window-dressing” can have on quarter-end repo rates. As the BIS wrote in a March 2024 working paper, “Banks’ market activity is commonly observed to contract around period-end dates…window-dressing is defined as the temporary reduction in market activity and balance sheet items by banks in anticipation of period-end reporting dates in order to appear safer or less systematically important than they may actually be.”

What’s the practical difference between central bank lending facilities and QE?

Some readers may be wondering about the potential implications if indeed central banks emphasize their lending facilities/programs over outright securities purchases for the foreseeable future. Central banks’ asset purchases change assets’ term premia, whereas lending facilities have no such impact. (The term premium is the excess return that an investor earns from committing to hold a long-term bond instead of a series of shorter-term bonds.) Isabel Schnabel of the ECB acknowledged in her aforementioned speech that QE likely contributed to the compression of risk premia. “Price-earnings ratios in stock markets across advanced economies surged to record highs as major global central banks conducted QE before and after the pandemic. In 2021, before policy rates started to rise, spreads in many fixed income markets, including in the euro area, reached their lowest level since the global financial crisis.” Central bankers are aware of how substantial an impact QE can have on financial markets. The side effects, though, can be highly problematic, as Mr. Carstens at the BIS indicated.