An Update on Bank Lending to the Real Economy, or the Lack Thereof

Flat isn't the new up

I wrote a month ago (link and link) about stagnant bank lending to households and businesses, and that a disproportionate amount of banks’ loan growth is going to nondepository financial institutions (NDFIs) such as private credit firms, hedge funds and securitization vehicles. In the first post, I wrote that the idea behind Federal Reserve (Fed) interest rate reductions is that they’re supposed to spur borrowing and spending, but that there are many hopes/assumptions embedded in that line of thinking. One is that borrowing rates for households and businesses will respond to the Fed’s rate cuts in the direction that the Fed expects. Another is that banks will be willing and able to lend more to households and businesses if/when borrowing rates fall. Yet another is that households and businesses will be willing to borrow and spend more at lower rates. As Albert Einstein said, “Assumptions are made and most assumptions are wrong.”

The Fed has cut the fed funds rate by 75 basis points since September 18, yet there’s been no pickup in loans to households and businesses since, continuing the trend that prevailed before the cuts. Bank loans excluding those to NDFIs are up just 0.3% since then, while loans to NDFIs continue to grow at a far more rapid rate. Bank loans to NDFIs were up 13.4% YoY as of the week ending November 20, while all other loans were up just 1.3%. Year-to-date, bank loans ex. NDFIs are up 1.6%, the lowest growth rate in the past decade aside from the pandemic period. (I’m using “not seasonally adjusted” rather than seasonally adjusted data; there’s little difference between the two over time.)

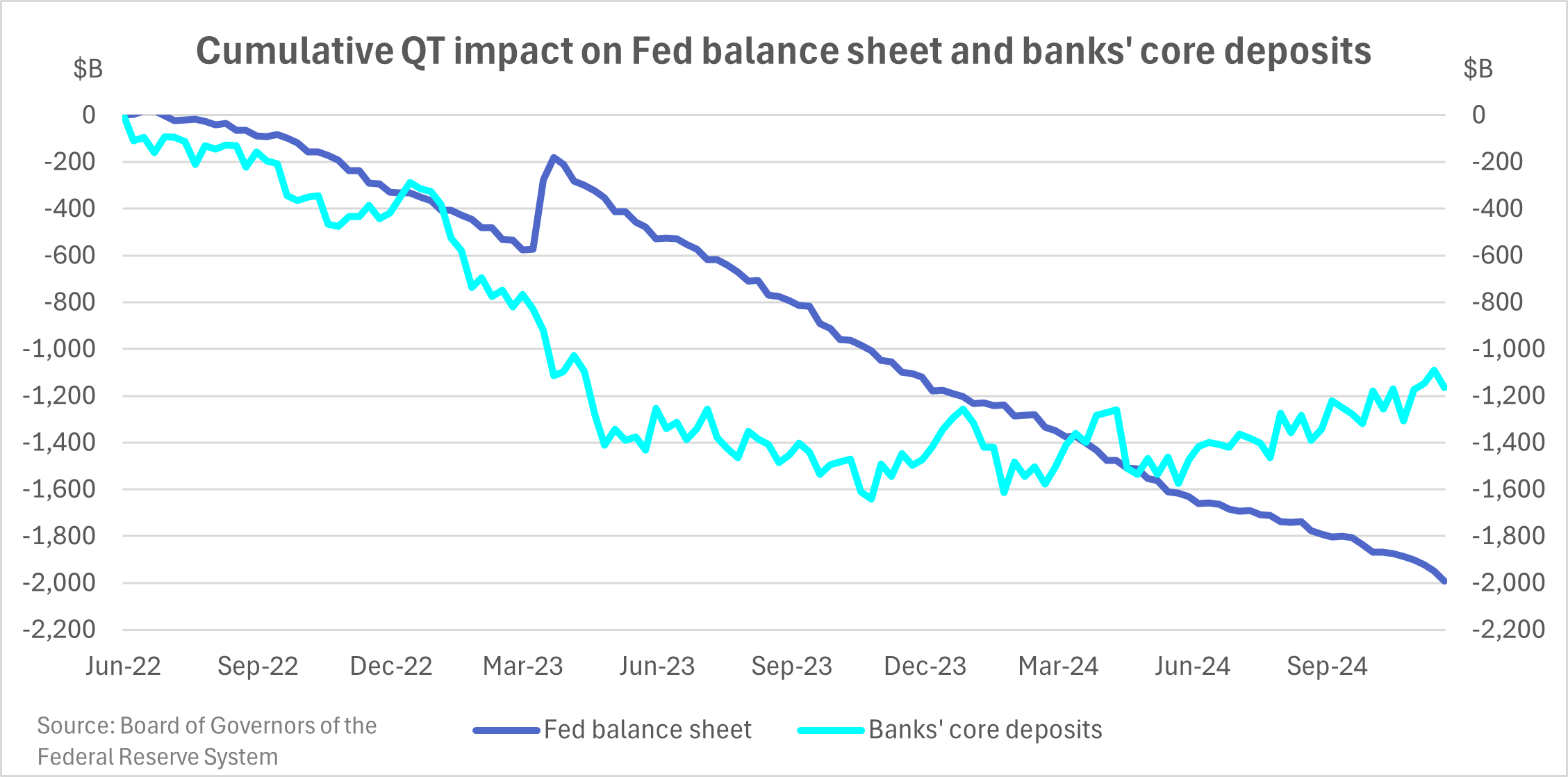

Why the lack of pickup in loans to Main Street since the Fed’s cuts? For starters, borrowing rates for many Americans have risen by roughly the same amount that the Fed cut: the 10-year Treasury yield is up ~50 basis points since the Fed started cutting, with 30-year fixed mortgage rates up even more. In addition, banks’ core deposits have barely risen, bearing in mind that deposit growth typically feeds loan growth. Just as bank loans ex. NDFIs are barely up this year, so too are their core deposits: they’re essentially unchanged from the end of last year (up just 0.6%) and from early 2021 levels. Since the Fed began its quantitative tightening (QT) program in June 2022, its balance sheet has shrunk by $2 trillion, while banks’ core deposits have fallen by nearly $1.2 trillion. (Core deposits are labeled “other” deposits in the Fed’s weekly H.8 releases.)

Why should one expect this state of affairs (the lack of loan growth to households and businesses) to change anytime soon? There’s no obvious reason to. Even if borrowing rates were to start falling, banks’ deposits show little sign of growing, and I think they’re unlikely to as long as QT continues. Along those lines, Fed officials have consistently maintained in recent months that bank reserves remain abundant, such that there’s no need to stop QT. As Dallas Fed President Lorie Logan said in late October, “At present, liquidity appears to be more than ample. Reserve balances are around $3.2 trillion, compared with around $1.7 trillion in early 2020. The economy and financial system have grown, and the dash for cash at the start of the pandemic as well as the banking stresses in March 2023 may have led banks to increase their demand for liquidity. Still, I think it’s unlikely banks’ liquidity demand has nearly doubled in half a decade.” (Bank reserves remained around $3.2 trillion as of last week, for those wondering.)

One favorable development for banks in recent months was falling interest rates, which had the effect of reducing banks’ (substantial) unrealized losses on their securities portfolios: according to FDIC call report data that BankRegData compiled and published on November 7, mark-to-market losses fell from $513 billion as of the end of 2024q2 to $364 billion as of the end of 2024q3, a $150 billion decline. For perspective, $150 billion is ~7% of banks’ Tier 1 capital as of 3Q, such that it’s a big number. From the end of 2Q to the end of 3Q, the 10-year Treasury yield fell from 4.34% to 3.8%, a 54 basis point decline. Since then, yields have risen back to just under 4.2%, such that much of the “progress” in 3Q has been undone. What does that mean? Banks’ unrealized losses are likely to rise substantially in 4Q barring a decline in interest rates from current levels, the most likely cause of which would be weak economic data. And why is this important for banks’ lending to households and businesses? Banks know they’re sitting on these unrealized losses, and are perhaps acting accordingly by limiting their asset/loan growth.

How are these trends reflected in the economy and markets? As I’ve written on numerous occasions, large, publicly-traded retailers, restaurant chains and consumer packaged goods (CPG) companies are reporting stagnant sales, with discretionary spending under considerable pressure. As banks lend increasingly more money to levered investment funds and not to the real economy, it’s logical to assume that the financial markets will grow disproportionately to corporate earnings, and that’s what we’ve seen over the past couple of years: ever-higher financial asset valuations. One such example: the Shiller P/E ratio has gone from 28x at the end of 2022 to 39x today, a 36% multiple expansion.