Bank Lending to NDFIs Continues to Surge; What's Going On?

Yet again, primary dealers are central to the story; Jamie Dimon explained it on Friday

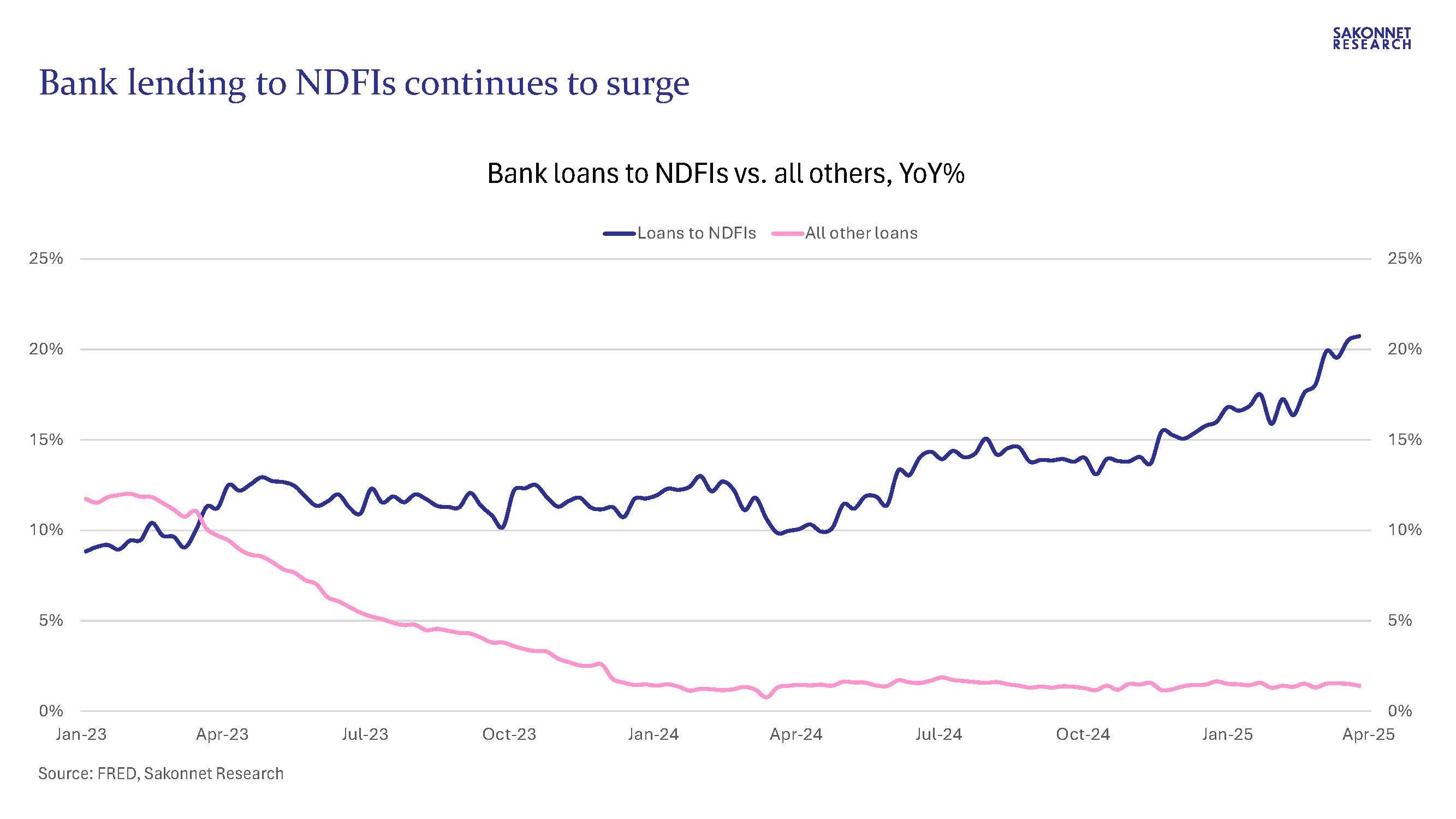

The Federal Reserve’s weekly H.8 release (the assets and liabilities of commercial banks), published on Friday at 4:15pm ET, highlighted a trend I’ve mentioned on numerous occasions in recent months: the rapid and accelerating growth in bank lending to levered nondepository financial institutions (NDFIs) compared to limited loan growth to the real economy (commercial and industrial loans, real estate loans and consumer loans). As of the week ending April 2, NDFI loans increased 21.7% vs. a year ago compared to all other loans up just 1.5% (see below). A year ago, NDFI loans were growing by 10%, which struck me as rapid then but which doesn’t hold a candle to what’s happening now. In fact, the recent boom in NDFI lending is part of a much larger trend.

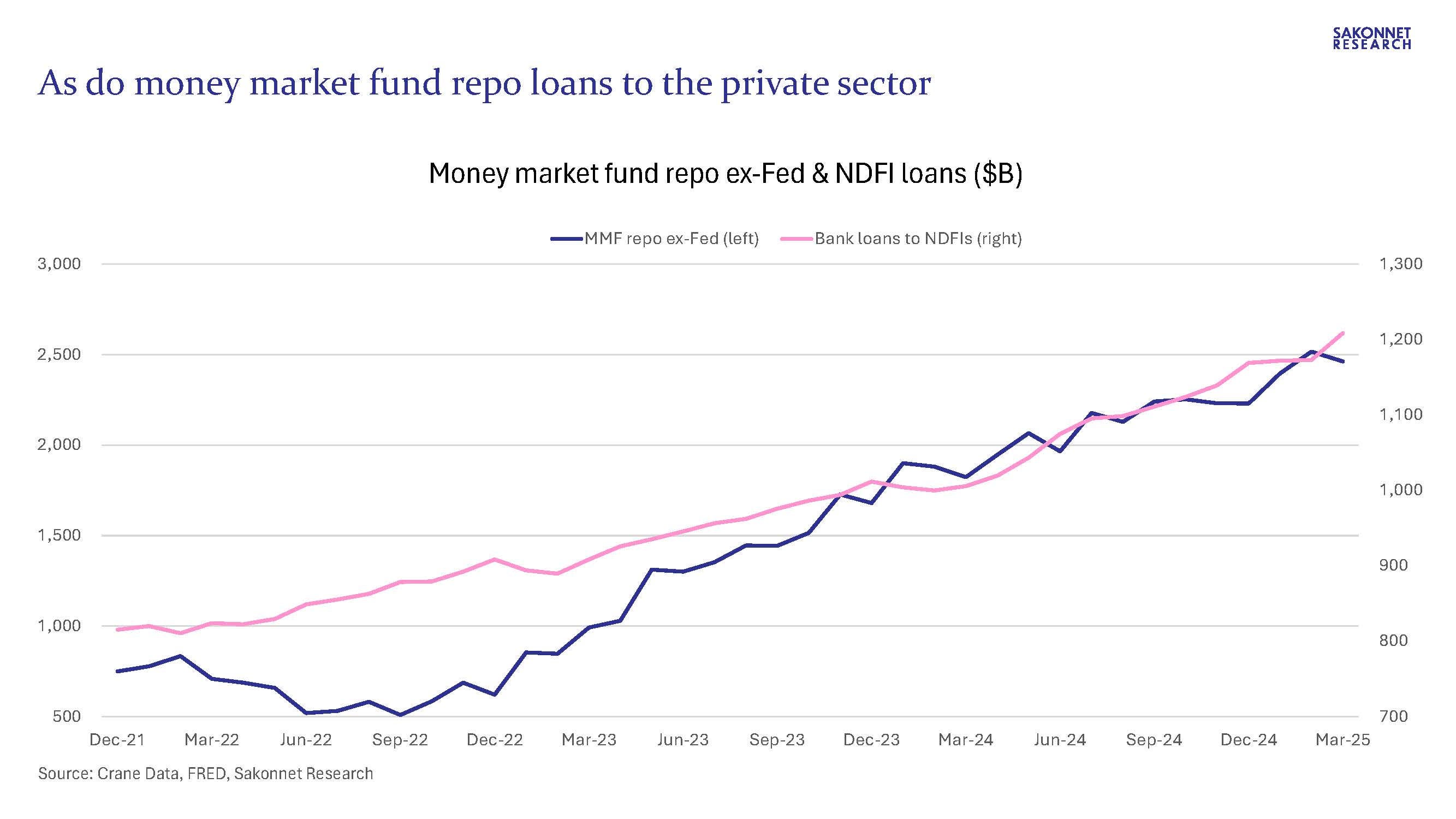

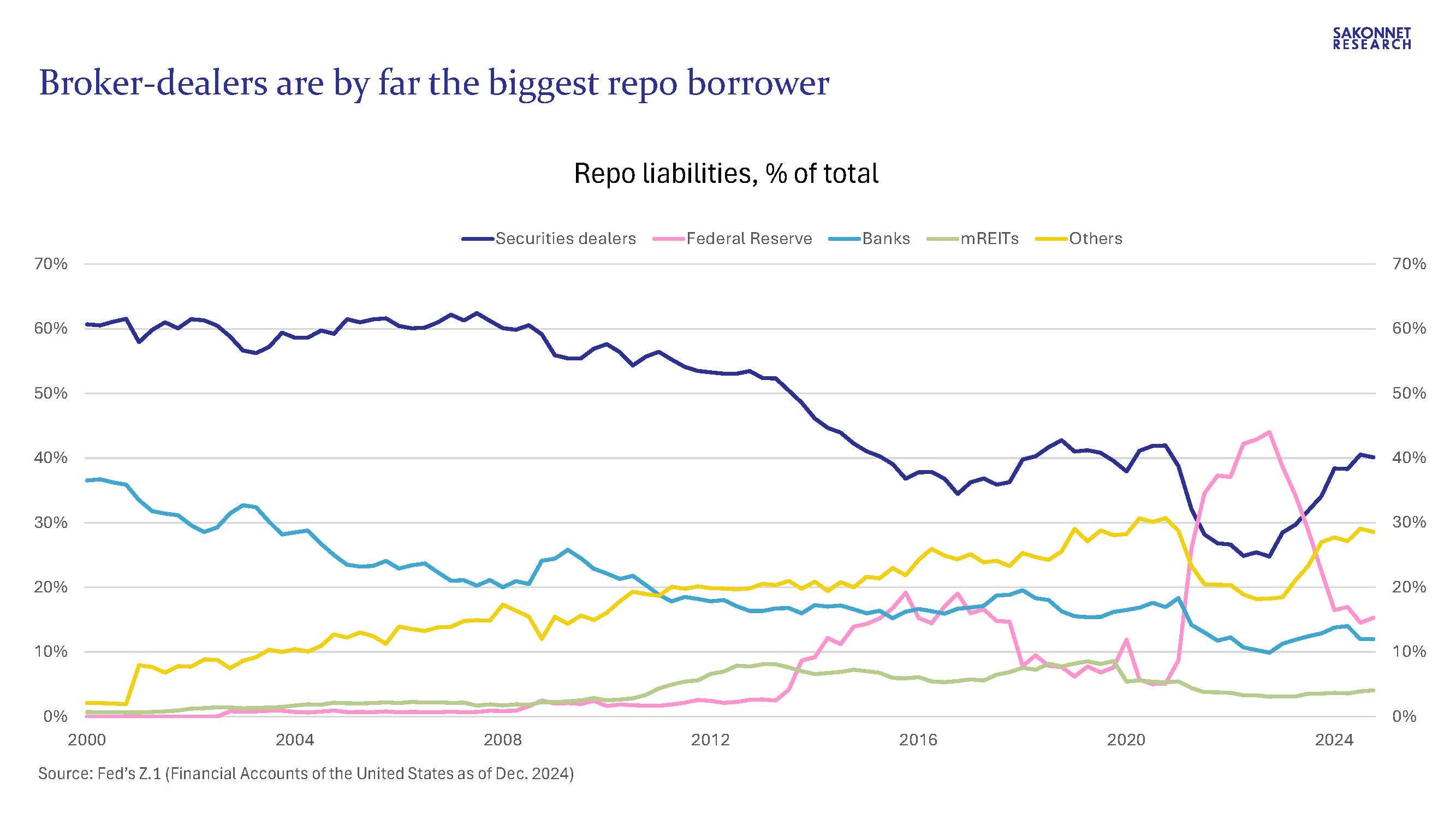

NDFIs include broker-dealers, hedge funds, private equity and credit funds, securitization vehicles, etc., essentially levered investment funds that own Treasurys, stocks and a variety of other assets. At the same time as NDFI lending has exploded, so too have money market funds’ (MMFs) repo loans to the private sector (the private sector defined in this case as all entities other than the Fed). A repo (repurchase agreement) is a short-term secured loan. Per Brookings’ research, “one party sells securities to another and agrees to repurchase those securities later at a higher price. The securities serve as collateral. The difference between the securities’ initial price and their repurchase price is the interest paid on the loan, known as the repo rate.” Who are the biggest repo borrowers, and by a wide margin? Broker-dealers, which accounted for 40% of repo liabilities as of December 2024 according to the Fed’s Z.1 release (see below). Broker-dealers are also among the NDFIs to which banks have been lending an increasing amount of money to; we don’t know broker-dealers’ share of NDFI borrowing because that information isn’t available, but I assume it’s high as is the case with repo liabilities.

Some perspective is in order regarding the scale of NDFI loans and MMF repo loans. NDFI loans have gone from $815 billion at the end of 2021 to $1.24 trillion today, up more than 50% in just over three years. And MMF repo loans (called holdings) ex-Fed have gone from $750 billion at the end of 2021 to nearly $2.5 trillion as of March 2025. The sum of the two has gone from $1.565 trillion to $3.67 trillion, up a whopping $2.1 trillion. Over the same period, total bank loans and leases only grew by $1.9 trillion. And bank loans and leases are a dramatically larger market than the combination of NDFI loans and MMF repo loans (the former was ~$11 trillion at the end of 2021, the latter just ~$1.5 trillion), such that the shift toward lending to financial market participants vs. the real economy has been an enormous one in percentage terms.

Two logical questions emerge. One is what’s happening with MMF assets such that their repo loans/holdings have been growing so dramatically? The other is, for which assets are broker-dealers providing financing given how much money they’re borrowing from MMFs and banks?

Regarding the first, according to Crane Data, U.S. MMF assets have grown by more than $2 trillion (42%) in just over three years, from $5.2 trillion as of December 2021 to $7.3 trillion as of March 2025. By comparison, U.S. commercial bank assets are up just $1.26 trillion since the end of 2021, and off of a vastly bigger base ($22.7 trillion). Treasurys and repo each account for ~39% of MMF holdings, such that as MMF assets go, so likely go their Treasury and repo holdings. Importantly, Treasurys outstanding grew by $6 trillion over the same period that MMF repo loans ex-Fed grew by $1.7 trillion and NDFI loans grew by $400 billion.

Why is that important? Here’s where the conversation shifts back to broker-dealers, specifically primary dealers. Primary dealers intermediate the Treasury and other securities markets, purchase Treasurys at auction, and act as a counterparty to the Fed. In other words, they’re a critical cog in the financial economy. As Treasury issuance has surged in recent years owing to the U.S. government’s chronic and enormous budget deficits, primary dealers have had to buy more of them; after all, primary dealers are required to participate in Treasury auctions, and in the secondary market they facilitate trading by taking bonds into their inventory and financing their clients’ purchases. As the NY Fed noted in a piece late last year, “Both dealers' primary and secondary market activities tend to increase with the amount of outstanding Treasury securities.”

There was much discussion last week when long-term U.S. government yields were spiking about the Treasury basis trade unwinding. Without getting into the nitty-gritty (I’ll let the Financial Times handle that), hedge funds buy Treasury bonds and sell Treasury futures, and the trade has exploded in popularity in recent years. The spreads are small, but according to FT Alphaville’s estimates, hedge funds typically use 50-100 times leverage on the capital invested. As the FT wrote, “In other words, just $10mn of capital can support as much as $1bn of Treasury purchases.”

And who provides that leverage? Primary dealers. Who provides leverage for hedge funds’ equity positions? Primary dealers. What happens when Treasurys, equities and/or other assets lose significant value as has happened in recent weeks? Hedge funds can and do suffer major losses, and dealers can and have as well. In fact, Bloomberg reported on Friday that one bond trader has lost $140 million in April and that another hedge fund team has been stopped out from trading after it accumulated $30 million in losses. In the collapse of Archegos Capital Management in 2021, dealers suffered over $10 billion of losses, partly as a result of which primary dealers’ equity fell by around $20 billion from 2021 to 2023 (from $150 billion to $130 billion).

When hedge funds start suffering losses, margin calls result, which leads to deleveraging. The FT reported that hedge funds were hit with the biggest margin calls since COVID after ‘Liberation Day’ tanked asset prices. And it’s not just hedge funds that are getting hit with margin calls: the FT reported on Friday that Angola (!) was hit with a nearly $200 million margin call by JPMorgan as the price of African bonds fell.

As I wrote about in my presentation last week, a substantial amount of leverage has built up in the financial system in recent years, facilitated by banks and primary dealers (which in many cases are affiliated with the same corporate entity, a bank-holding company). Leverage can and does go in both directions; we’ve seen signs of that over the past two weeks.

In that vein, the issue of primary dealers’ balance sheet constraints is an important one. Treasury issuance has grown dramatically in recent years, the Fed continues to slowly reduce its Treasury holdings, foreign official buyers have been doing the same in recent years (well before ‘Liberation Day’ and any lasting damage on foreign demand for Treasurys it caused), and the Treasury basis trade may have unwound to some extent in recent days, all of which begs the question of who the marginal Treasury buyers will be and at what price/yield. Primary dealers are already holding near-record amounts of Treasurys on their balance sheets, and it’s well known that their intermediation capacity hasn’t kept pace with Treasury issuance.

The Boston Fed recently published a timely piece along these lines. “Given the crucial role of primary dealers, policymakers and academics have pointed out the potential vulnerability of the Treasury market to changes in constraints on those dealers—such as changes involving banking capital regulation—that would affect their ability to efficiently intermediate the market (see, for example, Duffie 2018, 2020). This discussion has gained momentum in the wake of several recent disruptions in the Treasury market, significant accumulation of government debt in response to the COVID-19 crisis, and projections of further increasing federal deficits.” The authors continued, “Our analysis presents evidence that relaxing the SLR constraint—that is, lowering the required SLR—can cause an increase in dealers’ Treasury trading activity, especially among dealers affiliated with more constrained (lower-SLR) banks. This finding implies that the SLR requirement is indeed binding for some banks—that it constrains their Treasury positions to levels they would not otherwise choose.”

SLR is short for supplementary leverage ratio, which is a measure of a bank’s ability to absorb losses during periods of financial stress. As the Boston Fed piece explained, “…the Federal Reserve sets a minimum requirement for the SLR to help protect the stability of the banking system by preventing excessive leverage.” The denominator in the SLR calculation - total leverage exposure - includes primary dealers’ gross positions in securities: the sum of their long positions (the value of securities owned) and short positions (the value of securities they have promised to deliver). In April 2020, the Fed temporarily exempted Treasurys and reserves from the denominator of the SLR calculation for banks in response to the financial market dysfunction caused by the COVID crisis; that exemption expired a year later.

What may sound like an arcane topic is anything but, which is why JPMorgan Chase was asked about it on its 1Q results call on Friday. Part of Jamie Dimon’s response to a question about proposed SLR changes and the recent volatility in the Treasury market/weakening global demand for Treasurys (I’ve bolded certain sentences for emphasis): “And remember, it's not relief to the banks. It's relief to the markets. JPMorgan will be fine without an SLR change. The reason to change some of these things is so banks -- the big market makers can intermediate more in the markets. If they don't, if they do, spreads will come in, there'll be more active traders. If they don't, the Fed will have to intermediate, which I think is just a bad policy idea. Every time there's a kerfuffle in the markets, the Fed has to come in and intermediate. So they should make these changes. The point -- the reason why is when you have very lot of volatile markets and very widespread and low liquidity in treasuries, it affects all other capital markets.”